Owning a home is the cornerstone of the American dream, but for many, the 30-year mortgage feels more like a marathon with no finish line. If you are tired of seeing the bulk of your monthly check go toward interest rather than equity, you’ve likely asked: “How quickly can I actually own this house outright?”

Our pay off mortgage calculator is designed to answer that exact question. By analyzing your current principal balance, interest rate, and potential extra pay off mortgage calculator payments, this tool provides a clear roadmap to financial freedom. Whether you want to become debt-free in a decade or are looking for a how to pay off mortgage in 5 years calculator, the data below will help you strategize your path to a $0 balance.

How to Use the Mortgage Payoff Calculator

To get the most accurate results from this home loan payoff calculator, you’ll need a few pieces of data from your most recent mortgage statement. Understanding these variables is the first step in mastering your personal finance issues.

1. Current Loan Balance

This is your remaining pay off mortgage calculator input. Do not use your original purchase price; instead, look for the “Current Principal Balance” on your statement.

2. Interest Rate

Input your annual percentage rate (APR). Even a 0.5% difference can drastically change your mortgage interest savings calculator results.

3. Monthly Principal and Interest Payment

Exclude your property taxes and homeowners insurance (escrow) from this field. The calculator specifically focuses on the principal and interest payment to determine the amortization timeline.

4. Additional Monthly Principal

This is where the magic happens. By adding principal payments to pay off mortgage calculator fields, you can see exactly how many years you shave off your loan term.

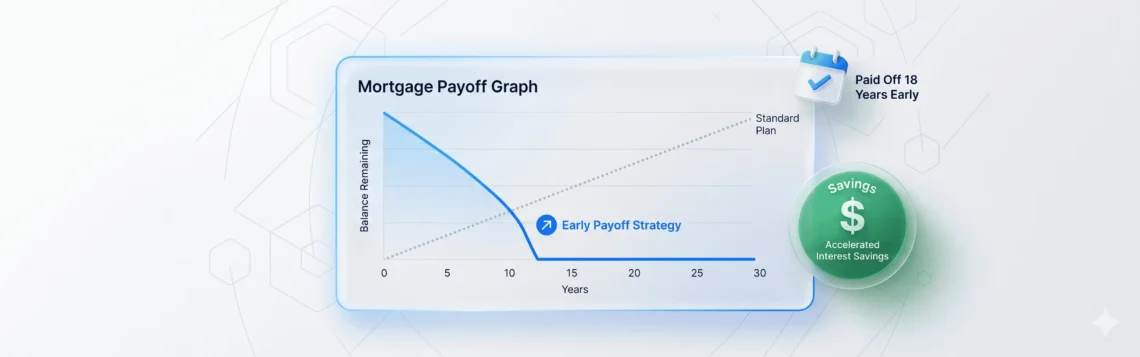

How Much Can You Save by Paying Off Your Mortgage Early?

Most homeowners don’t realize that in the first 10 years of a 30-year loan, the majority of their mortgage payment goes toward interest, not the house itself. By using an extra principal payment pay off mortgage calculator, you can flip the script.

The Impact of Extra Payments (Table)

Assumes a $300,000 balance at 6.5% interest with 25 years remaining.

Extra Monthly Payment

Total Interest Saved

Years Shaved Off Loan

New Payoff Date

$0 (Standard)

$0

0 Years

25 Years

$100

$42,450

3 Years, 2 Months

21 Years, 10 Months

$300

$102,120

7 Years, 9 Months

17 Years, 3 Months

$500

$141,800

10 Years, 11 Months

14 Years, 1 Month

As shown, even a modest additional principal calculator mortgage entry of $300 can save you over six figures in interest. This is money that stays in your retirement fund rather than the bank’s pocket.

Strategies to Pay Off Your Mortgage Faster

If you’ve used the mortgage payoff estimator and want to accelerate your timeline, consider these proven strategies:

Making Extra Principal Payments

The most straightforward way to use an additional payment mortgage calculator strategy is to simply add a set amount to your monthly check. Ensure you specify to your servicer that the extra funds should be applied to the principal balance, not the next month’s payment.

The Bi-Weekly Payment Hack

By paying half of your monthly mortgage every two weeks, you end up making 26 half-payments. This equals 13 full payments a year. This “extra” payment can shorten a 30-year mortgage by roughly 4 to 6 years without you ever feeling a major “pinch” in your budget.

Recasting vs. Refinancing

If you have a lump sum (like an inheritance or bonus), a mortgage paydown calculator might suggest a “recast.” For a small fee, the bank keeps your current interest rate but recalculates your monthly payment based on the new, lower balance. Unlike refinancing, there are no closing costs.

How to Calculate Your Mortgage Payoff Amount

Many users confuse their “current balance” with their mortgage loan payoff amount. If you are planning to write a final check today, you need to figure out mortgage payoff amount precisely.

Daily Interest (Per Diem): Interest on mortgages usually accrues daily. If you pay on the 15th of the month, you owe 15 days of interest that hasn’t been billed yet.

Statement Lag: Your monthly statement balance is often a “snapshot” from weeks ago.

Escrow Buffers: You may have a credit in your escrow account for taxes that will be refunded after the house payoff is complete.

To determine mortgage payoff amount officially, you must request a “Payoff Statement” from your lender. This document is legally binding and includes the exact amount needed to satisfy the lien down to the penny. (Pay off Mortgage Calculator 100% accurate)

Is Paying Off Your Mortgage Early the Right Move?

Before you use every cent of your savings on a mortgage repayment planner, consider your individual circumstances.

Opportunity Cost: If your mortgage interest rate is 3% and the stock market returns 8%, a mortgage payoff calculator might show savings, but investing the extra cash could increase your net worth more.

Liquidity: Once you put money into your home’s equity, it is “trapped” until you sell the house or take out a HELOC.

Prepayment Penalty: Some older or non-conforming loans have a prepayment penalty. Check your original loan estimate before using a house payoff calculator to plan an aggressive exit.

Frequently Asked Questions (FAQ) – Pay Off Mortgage Calculator

How do I calculate my mortgage payoff?

To calculate mortgage payoff, take your current principal balance and add the interest that will accrue between your last payment and your intended payoff date. For the most accurate number, use a mortgage payoff amount calculator or request a payoff quote from your bank.

Can I pay off my mortgage in 5 years?

Yes, but it requires a significant extra principal calculator for mortgage strategy. For example, on a $200,000 balance at 7%, you would need to pay approximately $3,960 per month to be debt-free in 60 months.

When will my mortgage be paid off if I pay an extra $200 a month?

On a standard $250,000 30-year loan at 6%, an extra $200 per month will shave roughly 8 years off your loan and save you over $80,000 in interest. Use our mortgage calculator payoff date feature to see your specific date.

Does an extra payment go directly to principal?

Usually, yes, but you must verify with your lender. Some banks default extra funds to “pre-pay” the next month’s interest. Always mark the extra funds as “Principal Only” to ensure your mortgage paydown calculator results stay on track.

Final Thoughts: Your Path to a Mortgage-Free Life

Using a pay off mortgage calculator is about more than just numbers; it’s about peace of mind. Every dollar you send toward your principal today is a guaranteed “return on investment” equal to your interest rate.

While the math of an amortization payoff calculator is clear, the psychological benefit of owning your home outright is immeasurable. Start small—even an extra $50 a month can change your financial future.

Disclaimer: The information provided by this pay off mortgage calculator and guide is for illustrative purposes only. The results are hypothetical and may not apply to your individual circumstances. Mortgage terms, prepayment penalties, and interest calculations vary by lender. We recommend you seek personalized advice from qualified professionals or your financial advisor before making significant changes to your mortgage loan repayment strategy. All information and interactive calculators are provided as a self-help tool for your independent use.

Real-Time CPM Analysis – CPM Calculator Marketing Cost $ Total Impressions # Market Score: Calculated CPM $0.00 Total Cost: Total Impressions: Budget Warning: Your CPM is higher than the 2026 industry average. This could be due to poor targeting or creative fatigue. Hire an Expert Marketer to Optimize → Successfully managing a digital marketing budget requires more than just creativity; it demands precise financial oversight of your ad spend. Whether you are running a total campaign on Meta or managing ad impressions across Google Display, understanding your CPM rate is the difference between a high-ROI campaign and a wasted budget. Our professional CPM calculator allows you to instantly calculate cpm, determine your campaign cost, or forecast the total impressions needed to reach your marketing goals. What is CPM? Understanding Cost Per Mille In the world of media buying, CPM stands for Cost Per Mille—”mille” being the Latin word for one thousand. Therefore, CPM is the cost per thousand impressions. This metric represents what an advertiser pays for every 1,000 impressions their advertisement receives. Unlike Cost Per Click (CPC), where you pay for user engagement, CPM focuses on brand awareness metrics and inventory pricing. It is the standard advertising calculator metric for measuring the reach and visibility of a total campaign. Why CPM Still Matters in 2026 Even with the rise of performance-based bidding, CPM remains a foundational entity in marketing budget efficiency. As the industry shifts toward privacy-preserving auctions like the Privacy Sandbox, tracking the number of impressions and their associated costs has become even more critical for budget allocation. The CPM Formula: How to Calculate Manually While our online cpm calculator handles the math instantly, every digital marketer should understand the cpm calculation logic. To calculate the cpm, you divide the total cost of the ad by the number of impressions, then multiply by 1,000. The Standard CPM Formula: How to calculate impressions from CPM: If you already have a target cpm rate and a fixed ad spend, you can reverse the cpm formula to find your estimated impressions: CPM vs. CPC vs. CPA: Which Pricing Model is Best? Choosing the right advertising campaign model depends on your Return on Ad Spend (ROAS) goals. Metric Full Name Primary Goal Best For CPM Cost Per Mille Awareness High Reach & Brand Visibility CPC Cost Per Click Traffic Lead Generation & Sales CPA Cost Per Acquisition Conversions Direct Response & ROI Expert Insight: A low CPM is often a “top-of-funnel” victory. While it looks great for maximizing total numbers, it doesn’t always guarantee high-quality traffic. Always calculate your eCPM (effective CPM) to understand the true value of your ad spend Industry Benchmarks for 2026: What is a “Good” CPM? A “good” CPM is highly subjective and depends on your inventory pricing and platform. In 2026, we are seeing significant shifts due to dynamic bidding models like Model Predictive Control (MPC). 5 Proven Strategies to Lower Your CPM If your cpm tracker shows rising costs, use these expert-level strategies to improve your marketing budget efficiency: Get More Impression with Low CPM – Hire An Expert The Impact of a Post-Cookie World on CPM The phase-out of third-party cookies in 2026 has created a massive pain point for advertisers, leading to a nearly 30% reduction in traditional publisher revenue. This has forced a shift toward semantic SEO and entity-based targeting. Our cpm calculator helps you navigate these changes by providing a clear view of your total campaign costs in this new, privacy-first landscape. Frequently Asked Questions (FAQ) You Can Check our other Tools here that make your life easier — All are Free Check our Tools

Prorated rent calculator Calculate your tenant’s prorated rent. Select tenant status Moving inMoving out Enter monthly rent Enter tenant move date Calculate Prorated rent for the month of $0.00 0 days * $0.00 per day Reset Moving into a new apartment or transitioning out of a lease rarely happens exactly on the first of the month. This is where a prorated rent calculator becomes an essential tool for both landlords and tenants. Instead of paying for a full month you aren’t fully occupying, you only pay for the specific number of days you live in the property. In this guide, we will break down the prorated rent meaning, show you the exact math behind the rent proration calculator, and help you ensure your next rent payment is accurate to the penny. What is Prorated Rent? Prorated rent is the adjusted amount of rent a tenant pays when they occupy a rental unit for only a portion of the billing cycle. Whether you are moving in on the 10th or moving out on the 20th, prorating ensures that the monthly rent amount is divided fairly based on actual usage. Why Do You Need to Prorate Rent? How to Calculate Prorated Rent (Step-by-Step) To calculate the prorated amount manually, follow these four professional steps used by property management experts: Step 1: Determine the Monthly Rent Amount This is the total cost of rent for a full, uninterrupted month as stated in your lease agreement. Step 2: Identify the Number of Days in the Month This is a crucial step because prorated rent 30 or 31 days logic changes the daily rate. Some landlords use a flat 30-day average, while others use the actual calendar days. Step 3: Calculate the Daily Rent Amount Divide your total monthly rent by the number of days in the month. Step 4: Multiply by the Days of Occupation Finally, multiply the daily rent by the total days the tenant is occupying the property. Common Proration Methods Not all rent prorate calculators use the same logic. Depending on your state laws or lease terms, you might use: Prorated Rent Calculator for Move-In and Move-Out When a tenant moves in, the calculation typically starts from the move-in date through the end of that month. For a move-out prorated rent scenario, the calculation covers the 1st of the month until the keys are handed over. Example Calculation: Prorated Rent Calculator for Landlords: Legal and Professional Tips For landlords, calculating rent correctly is about more than just the math; it’s about maintaining a professional relationship with the tenant moves in. Incorrectly calculating the prorated amount can lead to disputes, delayed rent payments, or even legal issues in tenant-friendly jurisdictions. 1. State Laws and Lease Consistency Always ensure that the method you use to calculate the prorated amount is clearly stated in your lease agreement. Some states have specific regulations regarding whether you must use the actual days in the month or a standard 30-day billing cycle. If your lease is silent on the matter, using the actual calendar days (the “Actual/Actual” method) is generally considered the fairest approach in court. 2. Handling the Security Deposit Remember that the security deposit is almost always a full monthly rent amount, regardless of whether the first month is prorated. Do not prorate rent and the security deposit together; they are separate financial entities. The prorated amount only applies to the occupying the property period. 3. Clear Documentation When you provide the prorated rent amount to your tenant, provide a written breakdown. Show them the daily rent amount, the number of days being charged, and the total. This transparency reduces friction during the move-in or move-out date transition. Edge Cases: When Proration Gets Complicated While a rent calculator handles most situations, certain scenarios require a more nuanced understanding of prorate rent logic. Leap Years and February In a leap year, February has 29 days. If a tenant is moving in on February 15th, your daily rent amount will be lower than in a standard 28-day February. Using a prorating calculator that accounts for the specific year is vital for accuracy. Mid-Month Rent Increases If a rent increase takes effect on the 15th of the month, you will essentially need to prorate two different rates. Utilities and Extra Fees Does your rental include a flat fee for utilities or parking? These should generally be prorated alongside the base rent. However, one-time fees (like a pet deposit or application fee) are never prorated. Moving Out Early: Do You Get a Refund? A common question among renters is whether they can prorate rent if they choose to leave a few days before their lease officially ends. Generally, if you have a lease that ends on the 31st but you choose to move out on the 25th for your own convenience, the landlord is not legally obligated to prorate rent for those remaining 6 days. Proration usually only occurs when the lease itself begins or ends mid-month. However, if a new tenant moves in immediately after you vacate, some jurisdictions prevent the landlord from “double-dipping” (collecting rent from two people for the same days). In this case, you may be entitled to a prorated rent amount refund. Why Accuracy Matters for Your Credit and Rental History Your history of consistent rent payment is often reported to credit bureaus or used by future property management companies as a reference. An unpaid “difference” of $20 caused by a math error in how to calculate pro rata rent could potentially show up as a delinquency. Using a professional prorated rent calculator move in tool ensures that both parties agree on the exact figure, leaving no room for “he-said-she-said” during the final walkthrough. Frequently Asked Questions (FAQs)

Steps to Miles Calculator Steps To Miles Calculator Gender MaleFemale Height (cm) Number of Steps Stride Length (inches) (Optional) Calculate Distance Results 0.00 Miles 0.00 Kilometers 0 Estimated Calories Burned Want to reduce your weight? Try our advanced Weight Loss Planner! Weight Loss Planner → Whether you are tracking your daily movement on a Fitbit, Apple Watch, or a simple pedometer, the question is always the same: how many miles is that? Understanding your steps walked is the first step toward hitting your fitness goals, but the number of steps it takes to cover a mile isn’t the same for everyone. In this comprehensive guide, we will use the miles calculator logic to help you convert steps to miles with precision, accounting for stride length, average step size, and individual physical markers like length height ratios. The Simple Formula: How to Convert Steps to Miles At its most basic level, the distance you travel depends on your step length. On average, it takes approximately 2,000 steps to walk one mile. However, for a more accurate calculation, we look at the standard measurement of a mile: 5,280 feet. To find your specific distance, you use the mile divide method: Pro Tip: If you don’t know your stride, the industry average step is roughly 2.2 to 2.5 feet. Calculating Your Step Length and Stride Length To use a step to mile calculator effectively, you must understand the difference between a single step and a stride. How Your Height Affects Distance Your length height (your total height) is the biggest indicator of your step. A taller person has a longer single step, meaning they require fewer steps per mile. Steps to Miles Conversion Table: Quick Reference If you don’t want to do the math manually, use this chart based on an average stride length of 2.5 feet. Number of Steps Distance in Miles (Approx.) Kilometers (Approx.) 1,000 steps 0.5 miles 0.8 km 2,000 steps 1.0 mile 1.6 km 3,000 steps 1.5 miles 2.4 km 4,000 steps 2.0 miles 3.2 km 5,000 steps 2.5 miles 4.0 km 8,000 steps 4.0 miles 6.4 km 10,000 steps 5.0 miles 8.0 km 12,000 steps 6.0 miles 9.6 km 15,000 steps 7.5 miles 12.1 km 20,000 steps 10.0 miles 16.1 km Deep Dive: The 10,000 Steps Benchmark The “10,000 steps” goal is a worldwide fitness phenomenon. But how far is walking a mile five times over? For most people, 10,000 steps equates to roughly 5 miles. However, if you are running, your step length increases significantly. When running, you might hit 10,000 steps and find you have covered closer to 6 or 7 miles because your feet stay off the ground longer and cover more distance per single step. What about higher volumes? – Steps To Miles Calculator How to Calculate Your Personal Steps per Mile If you want to move beyond the average step and get clinical accuracy, follow these steps: Gender and Fitness Levels: Why it Matters When users search for how many miles is 17,000 steps for a woman, they are looking for biological accuracy. Generally, women have a shorter step length than men of the same height due to pelvic structure and muscle distribution. For men, who may have an average step closer to 2.6 or 2.7 feet, those same 17,000 steps could easily cross the 8.5-mile threshold. Conclusion: Making Every Step Count Understanding your steps converted to miles helps turn abstract numbers on a screen into tangible achievements. Whether you are aiming for 10,000 steps or pushing toward 20,000 steps, knowing your step length and the mile divide formula allows you to plan your routes and your fitness goals with confidence. Next time you look at your watch and see 12,000 steps, you’ll know you didn’t just “walk”—you covered six miles of ground, burned hundreds of calories, and moved closer to a healthier version of yourself.

Real-Time CPM Analysis – CPM Calculator Marketing Cost $ Total Impressions # Market Score: Calculated CPM $0.00 Total Cost: Total Impressions: Budget Warning: Your CPM is higher than the 2026 industry average. This could be due to poor targeting or creative fatigue. Hire an Expert Marketer to Optimize → Successfully managing a digital marketing budget requires more than just creativity; it demands precise financial oversight of your ad spend. Whether you are running a total campaign on Meta or managing ad impressions across Google Display, understanding your CPM rate is the difference between a high-ROI campaign and a wasted budget. Our professional CPM calculator allows you to instantly calculate cpm, determine your campaign cost, or forecast the total impressions needed to reach your marketing goals. What is CPM? Understanding Cost Per Mille In the world of media buying, CPM stands for Cost Per Mille—”mille” being the Latin word for one thousand. Therefore, CPM is the cost per thousand impressions. This metric represents what an advertiser pays for every 1,000 impressions their advertisement receives. Unlike Cost Per Click (CPC), where you pay for user engagement, CPM focuses on brand awareness metrics and inventory pricing. It is the standard advertising calculator metric for measuring the reach and visibility of a total campaign. Why CPM Still Matters in 2026 Even with the rise of performance-based bidding, CPM remains a foundational entity in marketing budget efficiency. As the industry shifts toward privacy-preserving auctions like the Privacy Sandbox, tracking the number of impressions and their associated costs has become even more critical for budget allocation. The CPM Formula: How to Calculate Manually While our online cpm calculator handles the math instantly, every digital marketer should understand the cpm calculation logic. To calculate the cpm, you divide the total cost of the ad by the number of impressions, then multiply by 1,000. The Standard CPM Formula: How to calculate impressions from CPM: If you already have a target cpm rate and a fixed ad spend, you can reverse the cpm formula to find your estimated impressions: CPM vs. CPC vs. CPA: Which Pricing Model is Best? Choosing the right advertising campaign model depends on your Return on Ad Spend (ROAS) goals. Metric Full Name Primary Goal Best For CPM Cost Per Mille Awareness High Reach & Brand Visibility CPC Cost Per Click Traffic Lead Generation & Sales CPA Cost Per Acquisition Conversions Direct Response & ROI Expert Insight: A low CPM is often a “top-of-funnel” victory. While it looks great for maximizing total numbers, it doesn’t always guarantee high-quality traffic. Always calculate your eCPM (effective CPM) to understand the true value of your ad spend Industry Benchmarks for 2026: What is a “Good” CPM? A “good” CPM is highly subjective and depends on your inventory pricing and platform. In 2026, we are seeing significant shifts due to dynamic bidding models like Model Predictive Control (MPC). 5 Proven Strategies to Lower Your CPM If your cpm tracker shows rising costs, use these expert-level strategies to improve your marketing budget efficiency: Get More Impression with Low CPM – Hire An Expert The Impact of a Post-Cookie World on CPM The phase-out of third-party cookies in 2026 has created a massive pain point for advertisers, leading to a nearly 30% reduction in traditional publisher revenue. This has forced a shift toward semantic SEO and entity-based targeting. Our cpm calculator helps you navigate these changes by providing a clear view of your total campaign costs in this new, privacy-first landscape. Frequently Asked Questions (FAQ) You Can Check our other Tools here that make your life easier — All are Free Check our Tools

Prorated rent calculator Calculate your tenant’s prorated rent. Select tenant status Moving inMoving out Enter monthly rent Enter tenant move date Calculate Prorated rent for the month of $0.00 0 days * $0.00 per day Reset Moving into a new apartment or transitioning out of a lease rarely happens exactly on the first of the month. This is where a prorated rent calculator becomes an essential tool for both landlords and tenants. Instead of paying for a full month you aren’t fully occupying, you only pay for the specific number of days you live in the property. In this guide, we will break down the prorated rent meaning, show you the exact math behind the rent proration calculator, and help you ensure your next rent payment is accurate to the penny. What is Prorated Rent? Prorated rent is the adjusted amount of rent a tenant pays when they occupy a rental unit for only a portion of the billing cycle. Whether you are moving in on the 10th or moving out on the 20th, prorating ensures that the monthly rent amount is divided fairly based on actual usage. Why Do You Need to Prorate Rent? How to Calculate Prorated Rent (Step-by-Step) To calculate the prorated amount manually, follow these four professional steps used by property management experts: Step 1: Determine the Monthly Rent Amount This is the total cost of rent for a full, uninterrupted month as stated in your lease agreement. Step 2: Identify the Number of Days in the Month This is a crucial step because prorated rent 30 or 31 days logic changes the daily rate. Some landlords use a flat 30-day average, while others use the actual calendar days. Step 3: Calculate the Daily Rent Amount Divide your total monthly rent by the number of days in the month. Step 4: Multiply by the Days of Occupation Finally, multiply the daily rent by the total days the tenant is occupying the property. Common Proration Methods Not all rent prorate calculators use the same logic. Depending on your state laws or lease terms, you might use: Prorated Rent Calculator for Move-In and Move-Out When a tenant moves in, the calculation typically starts from the move-in date through the end of that month. For a move-out prorated rent scenario, the calculation covers the 1st of the month until the keys are handed over. Example Calculation: Prorated Rent Calculator for Landlords: Legal and Professional Tips For landlords, calculating rent correctly is about more than just the math; it’s about maintaining a professional relationship with the tenant moves in. Incorrectly calculating the prorated amount can lead to disputes, delayed rent payments, or even legal issues in tenant-friendly jurisdictions. 1. State Laws and Lease Consistency Always ensure that the method you use to calculate the prorated amount is clearly stated in your lease agreement. Some states have specific regulations regarding whether you must use the actual days in the month or a standard 30-day billing cycle. If your lease is silent on the matter, using the actual calendar days (the “Actual/Actual” method) is generally considered the fairest approach in court. 2. Handling the Security Deposit Remember that the security deposit is almost always a full monthly rent amount, regardless of whether the first month is prorated. Do not prorate rent and the security deposit together; they are separate financial entities. The prorated amount only applies to the occupying the property period. 3. Clear Documentation When you provide the prorated rent amount to your tenant, provide a written breakdown. Show them the daily rent amount, the number of days being charged, and the total. This transparency reduces friction during the move-in or move-out date transition. Edge Cases: When Proration Gets Complicated While a rent calculator handles most situations, certain scenarios require a more nuanced understanding of prorate rent logic. Leap Years and February In a leap year, February has 29 days. If a tenant is moving in on February 15th, your daily rent amount will be lower than in a standard 28-day February. Using a prorating calculator that accounts for the specific year is vital for accuracy. Mid-Month Rent Increases If a rent increase takes effect on the 15th of the month, you will essentially need to prorate two different rates. Utilities and Extra Fees Does your rental include a flat fee for utilities or parking? These should generally be prorated alongside the base rent. However, one-time fees (like a pet deposit or application fee) are never prorated. Moving Out Early: Do You Get a Refund? A common question among renters is whether they can prorate rent if they choose to leave a few days before their lease officially ends. Generally, if you have a lease that ends on the 31st but you choose to move out on the 25th for your own convenience, the landlord is not legally obligated to prorate rent for those remaining 6 days. Proration usually only occurs when the lease itself begins or ends mid-month. However, if a new tenant moves in immediately after you vacate, some jurisdictions prevent the landlord from “double-dipping” (collecting rent from two people for the same days). In this case, you may be entitled to a prorated rent amount refund. Why Accuracy Matters for Your Credit and Rental History Your history of consistent rent payment is often reported to credit bureaus or used by future property management companies as a reference. An unpaid “difference” of $20 caused by a math error in how to calculate pro rata rent could potentially show up as a delinquency. Using a professional prorated rent calculator move in tool ensures that both parties agree on the exact figure, leaving no room for “he-said-she-said” during the final walkthrough. Frequently Asked Questions (FAQs)

Steps to Miles Calculator Steps To Miles Calculator Gender MaleFemale Height (cm) Number of Steps Stride Length (inches) (Optional) Calculate Distance Results 0.00 Miles 0.00 Kilometers 0 Estimated Calories Burned Want to reduce your weight? Try our advanced Weight Loss Planner! Weight Loss Planner → Whether you are tracking your daily movement on a Fitbit, Apple Watch, or a simple pedometer, the question is always the same: how many miles is that? Understanding your steps walked is the first step toward hitting your fitness goals, but the number of steps it takes to cover a mile isn’t the same for everyone. In this comprehensive guide, we will use the miles calculator logic to help you convert steps to miles with precision, accounting for stride length, average step size, and individual physical markers like length height ratios. The Simple Formula: How to Convert Steps to Miles At its most basic level, the distance you travel depends on your step length. On average, it takes approximately 2,000 steps to walk one mile. However, for a more accurate calculation, we look at the standard measurement of a mile: 5,280 feet. To find your specific distance, you use the mile divide method: Pro Tip: If you don’t know your stride, the industry average step is roughly 2.2 to 2.5 feet. Calculating Your Step Length and Stride Length To use a step to mile calculator effectively, you must understand the difference between a single step and a stride. How Your Height Affects Distance Your length height (your total height) is the biggest indicator of your step. A taller person has a longer single step, meaning they require fewer steps per mile. Steps to Miles Conversion Table: Quick Reference If you don’t want to do the math manually, use this chart based on an average stride length of 2.5 feet. Number of Steps Distance in Miles (Approx.) Kilometers (Approx.) 1,000 steps 0.5 miles 0.8 km 2,000 steps 1.0 mile 1.6 km 3,000 steps 1.5 miles 2.4 km 4,000 steps 2.0 miles 3.2 km 5,000 steps 2.5 miles 4.0 km 8,000 steps 4.0 miles 6.4 km 10,000 steps 5.0 miles 8.0 km 12,000 steps 6.0 miles 9.6 km 15,000 steps 7.5 miles 12.1 km 20,000 steps 10.0 miles 16.1 km Deep Dive: The 10,000 Steps Benchmark The “10,000 steps” goal is a worldwide fitness phenomenon. But how far is walking a mile five times over? For most people, 10,000 steps equates to roughly 5 miles. However, if you are running, your step length increases significantly. When running, you might hit 10,000 steps and find you have covered closer to 6 or 7 miles because your feet stay off the ground longer and cover more distance per single step. What about higher volumes? – Steps To Miles Calculator How to Calculate Your Personal Steps per Mile If you want to move beyond the average step and get clinical accuracy, follow these steps: Gender and Fitness Levels: Why it Matters When users search for how many miles is 17,000 steps for a woman, they are looking for biological accuracy. Generally, women have a shorter step length than men of the same height due to pelvic structure and muscle distribution. For men, who may have an average step closer to 2.6 or 2.7 feet, those same 17,000 steps could easily cross the 8.5-mile threshold. Conclusion: Making Every Step Count Understanding your steps converted to miles helps turn abstract numbers on a screen into tangible achievements. Whether you are aiming for 10,000 steps or pushing toward 20,000 steps, knowing your step length and the mile divide formula allows you to plan your routes and your fitness goals with confidence. Next time you look at your watch and see 12,000 steps, you’ll know you didn’t just “walk”—you covered six miles of ground, burned hundreds of calories, and moved closer to a healthier version of yourself.